.png)

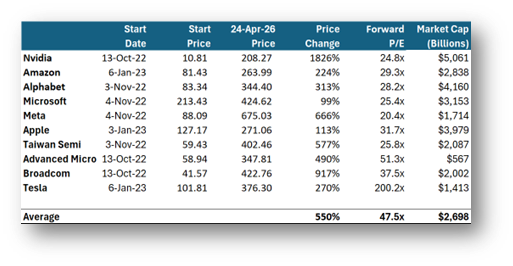

Well, it sure was an incredible wedding. And this honeymoon has been one for the ages. It hasn’t only been the most fun folks have had in a long while, it’s also been a wonderfully long celebration. And the party is still going on. Everyone’s still there. Nvidia is of course there. So are Amazon, Alphabet, and Microsoft. Same for Meta, Apple, Taiwan Semi, Advanced Micro, Broadcom, and even Tesla.

The celebration I am talking about is of course the AI revolution. Many folks are celebrating the share prices for these partygoers. Each of the attendees above are contributing to (or participating in) the AI revolution in different ways; and the trading volumes, valuation levels, and market caps for each of them have been more than impressive.

The brokers, naturally, have followed suit and created indices and products meant to mimic the performance of those companies above, plus a host of other AI-adjacent securities. Their goal, of course, is to capture flows from the retail investing community – a community that isn’t shy about their AI excitement.

And let’s just say the brokers have been pretty successful here. The BAI (iShare AI Innovation and Tech ETF) has averaged over $80 million of flows per day. Same for the Global X AI & Tech ETF. But the mack-daddy has been the Van Eck Semiconductor ETF, averaging over $3 billion a day in flows.

The whole of the stock market in France trades about $3 billion a day.

And this isn’t the first rodeo for the salesmen, or for transformative technologies and sectors, and their share prices.

Railroads

In the mid-19th century, railroads started transforming the landscape of England and Ireland; share prices were booming in the 1840s, and then severely busting in 1846. Just a few decades later, history repeated itself in the US. The building of a new nation, connecting from the Atlantic to the Pacific, garnered quite a lot of interest from speculators. And they were absolutely right about what would fundamentally happen. In 1862, we constructed 600 new miles of railroad in a single year across the country. Less than ten years later, in 1871 alone, we built over 7,000 miles of track.

But the stock and bond prices for the “players” got way ahead of themselves. And by 1873, the party was over. The value of the stocks and bonds of Northern Pacific, Union Pacific, and the Chicago and Rock Island Railroad plummeted. It was almost as if the bubble was needed to help finance the initial growth of the railroads in the first place, despite it costing investors dearly in the process.

Radio & Electric Utilities

By the 1920s, the future was now all about electricity. It was going to change the world. And it certainly did. The “Nvidia” of its day was RCA. In 1921, the shares traded for $1.50 per share. By 1929, they were trading for $570. By 1932, just three years later, they were trading back to $2.50 per share, down 98% from their peak.

The Internet

This one is a little more recent, and anyone GenX or older will surely remember it. The future was changing in front of everyone’s eyes, and the world was going nuts about anything-dot-com. Before the ‘90s, there were no social networks, no one shopped online, hardly anyone had a cell phone, and even fewer used this weird thing that grew out of the US Department of Defense called “the internet”.

Netscape and Yahoo listed in 1996, and Amazon had its IPO the following year. Meanwhile, Cisco, Lucent, and Nortel were selling the tools that everyone needed in the gold rush. Internet traffic was literally doubling every year (and Worldcom claimed it was doubling every quarter). Annual telecom CAPEX surged to over $200 billion (in today’s dollars). Global Crossing was building fiber across the oceans. Level 3 and Qwest were following suit.

Meanwhile, Worldcom bought MCI (the number two competitor to AT&T), AOL bought Netscape, and Cisco was buying everyone and their brother (literally 70 acquisitions in the 1990s, and 17 in 1999 alone).

That Amazon IPO was in May of 1997. Just over two years later, by December of 1999, the shares were up over 8,000%.

But then things changed. They changed in ways that were unfathomable to the hoards of investors who had piled into these “winners”. The honeymoon was over. And in many cases, divorce proceedings quickly started.

Within less than two years, by October of 2001, Amazon shares had fallen by 95%. From their peaks, CSCO plummeted 90%, eBay fell 79%, and Apple fell 83%. Heck, the Nasdaq itself (literally the entire index) dropped by 78% from peak-to-trough. Meanwhile, companies like Worldcom and Global Crossing just simply disappeared.

The Impact of Technological Revolution on Share Prices

Transformative technological innovations are very exciting. Even if the technology ultimately proves wonderfully successful, early euphoria can attract excessive short-term capital. It happened for the railroads, for radio and electricity, and it happened for the internet. At least historically, this setup has been the perfect recipe for speculative bubbles. One of the most interesting observations here is that the fundamental future predicted by the masses not only turned out to be precisely correct, but in some cases exceeded expectations. Yet the share prices of those participating in (or driving) the transformation were driven to wildly exaggerated share prices and market capitalizations. Thus, of course, even though the technology was “working”, the expected returns of these shares were reduced dramatically; and in many cases, they went negative.

That’s the nature of markets. And, just eyeballing things, it seems that the more revolutionary the technology, the more salaciously-hyperextended an asset bubble can become. So, with that, let’s have a quick look at those AI names that everyone loves these days.

First and foremost, there is Nvidia. Nvidia now has a market cap of over $5 trillion. That’s an awful lot of GPUs. And let’s broaden our example to the other names we mentioned above too. These 10 AI darlings below have a combined market cap of $27 trillion. In comparison, this itself is larger than the whole of Europe combined (a Europe with over 8,000 listed companies, including ASML at over $500 million).

We aren’t necessarily predicting the demise of any or all of these companies. By all accounts, most of them are incredibly well-run, high-quality businesses. We merely just want you to think about all this. Think about what exactly the share price is anticipating (or indeed requires) to generate further market cap gains from here. And think about the railroads, electricity, and the internet. Each was transformative, indeed. But from some point, none of them had a good marriage with their shareholders.

FOOTNOTES

DISCLAIMER

The views and opinions expressed in this post are those of the post’s author and do not necessarily reflect the views of Albert Bridge Capital, or its affiliates. This post has been provided solely for informational purposes and does not constitute an offer or solicitation of an offer or any advice or recommendation to purchase any securities or other financial instruments and may not be construed as such. The author makes no representations as to the accuracy or completeness of any information in this post or found by following any link in this post.

YOU MIGHT ALSO LIKE

Here We Go

I will try as always to be objective here, but maybe some bias will be revealed in the process. I hope not, and I am sure you will let me know if I do. Given how politically charged things can be these days, I am bound to upset someone. That is not my intention. Not one bit. I am trying to help. I’m trying to help our investors. I’m trying to help my friends. I’m trying to help myself.

Read More