'Til Death Do Us Part

One of the most interesting observations here is that the fundamental future predicted by the masses not only turned out to be precisely correct, but in some cases exceeded expectations. Yet the share prices of those participating in (or driving) the transformation were driven to wildly exaggerated share prices and market capitalizations.

Read More

AI and the Value of Information

The net excess return of all active investing in the aggregate is zero. This is true whether you use Claude, Gemini, or a slide rule.

Read More

Here We Go

I will try as always to be objective here, but maybe some bias will be revealed in the process. I hope not, and I am sure you will let me know if I do. Given how politically charged things can be these days, I am bound to upset someone. That is not my intention. Not one bit. I am trying to help. I’m trying to help our investors. I’m trying to help my friends. I’m trying to help myself.

Read More

On Stock-Picking in Volatile Environments

Whether stocks are heading dramatically north, or disastrously south, how do you know if it is overreaction and psychology, or actual economic fundamentals driving the share price? In other words, how do you know which is which?

Read More

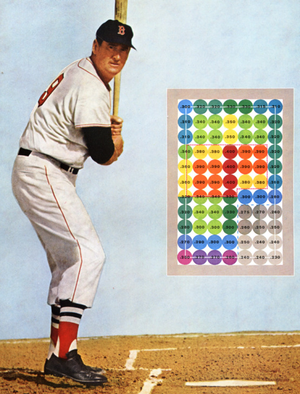

Stock Market History, Illuminated, 2024 Style

The Sustainability of US Equity Market Outperformance; a prologue.

Read More

Drew Chats with Matt Zeigler at The Intentional Investor and Epsilon Theory YouTube Channel

In the importance of culture, critique, and civility; and the impact some pretty impressive folks had on yours truly.

Read More

The Analyst's Code

There is no holy grail of investing, but there is a recipe for getting close...

Read More

Mean Reversion, or Extreme Aversion?

Why have US markets become more expensive than European ones? The answer will surprise you.

Read More

On the Legacy of Danny Kahneman

On the legacy of Danny Kahneman, and his impact on economics, finance, and our industry.

Read More

Volkswagen and Porsche SE are stuck in Wall Street’s pits. Stock investors, start your engines.

In our view, Porsche SE, with a recent 14 billion euro market cap (and trading over €40 billion a day), is one of the most underpriced, liquid, listed assets available to investors.

Read More

Drew Chats with Downtown Josh Brown

The impact of flows on security pricing, and investment opportunities.

Read More

Pods, Passive Flows, and Punters

The impact of pods, passive investment, and retail investors on security pricing.

Read More

Stock Market History Illuminated, 2023 Style

An illuminating color-coded infographic showing the distribution of US stock market returns by decade and annually for a long, long, time.

Read More

The Albert Bridge Factory

Define your process, and follow it, but don't completely ignore the regime we are in.

Read More

Hedge Fund Investing, Turnover, and Taxes

For taxable investors, the impact of taxes on long term post-tax returns really, really matters. But how much exactly do they matter? What sort of outperformance does one of your managers need to generate to offset the penalty of not buying and holding forever?

Read More

Stock Market History, Illuminated, 2022 Style

I’ve been keeping a graphic of the long-term performance of the US stock market for many years now, and I’ve been sharing this information in the histogram below. I think it does a reasonable job of revealing how long-term returns are manufactured and the tilts over time. I’ve color-chunked the data by decade to highlight decades of historical weakness as well as periods of strength. I’ve also added additional tables and charts which I think are interesting, and in some cases, stunning.

Read More

What Stands in the Way Becomes the Way

I don’t think that Aurelius, Frost or Zweig would disagree that the road less traveled might have a little more alpha in it.

Read More

Interest Rates and Growth Stocks

It's very possible, if not likely, that the move in growth stocks from 2017 through 2020 probably wasn’t caused or justified by a move in interest rates, but that people believed, and acted like, it was.

Read More

For Investors, a "Never-Sell" Mantra is a Song for Fools

On the misleading claims of Hendrik Bessembinder about diversification; and the convenient, post-hoc, and the spurious conclusion to always buy and hold.

Read More

A Conversation between Drew Dickson and Morgan Housel

A discussion between Drew Dickson of Albert Bridge Capital, Morgan Housel of The Collaborative Fund; moderated by Jamie Catherwood of O'Shaughnessy Asset Management

Read More

Conversation with Dr. Daniel Crosby on his Standard Deviations Podcast

Drew joins Dr. Daniel Crosby on the Standard Deviations podcast.

Read More

On the Disincentives of Investing in Public vs. Private Equity; and Implications for Pricing and Returns

Just as the public markets can be affected by short term flows, is it possible that private market valuations, and the periodic marks of particular private investments, have been affected by increasing allocation tilts toward private equity?

Read More

Why European Stocks Might Win

In an op-ed for Marketwatch, Drew explodes the myth about European companies, and reveals where he thinks the opportunities are today.

Read More

Finding Alpha in Europe

Drew and Toby chat about narrative-driven investing, Ben Graham's voting machine, behavioral explanations for stock mispricing, and managing a concentrated portfolio of investment ideas.

Read More

On the Relationship Between Gasoline Prices and Vehicle Demand

As it relates to demand for pickup trucks and SUVs, gasoline prices may not matter matter as much as they used to.

Read More

Sell in May and Go Away?

Turns out there may actually be something to the old Sell in May and Go Away adage - at least over the last 80+ years.

Read More

The Politics of Passive Investing

Most of us in the finance world are well aware of the evolution of “passive” equity investing over the years, and have witnessed its tremendous growth. Some of us have asked questions about it. We’ve asked is it all good? Is it mostly good? Are some aspects perhaps bad? Are some really bad?

Read More

If Growth Stocks Sell Off Will They Bring Value Stocks Down with Them?

Growth stocks crushed just about everything from 2017 through 2021. Not that they necessarily will, but if they do give back some or all of their gains, given their weightings, times will be tough for broader indices. But what about the value names within them, will they sell off in sympathy as well? Of course no one knows, including ourselves, but we take a quick look at behavior of value names as the tech bubble sold off from 2000 through 2002. This example may be worth some consideration.

Read More

Stock Market History, Illuminated

Some year-end charts and tables asking some big questions about what comes next.

Read More

Which One Are You?

So, if you are in the taxi, what is your first move (and you can’t say “do nothing”). Are you trimming or adding?

Read More

Was Ben Graham a Quant?

The short, and relatively unknown, paper is chock full of wonderful anecdotes and pearls of wisdom, but it was the interview portion that really caught my attention.

Read More

Do Short Term Flows Permanently Affect Share Prices?

I’d like to think that prices can get out of whack for some period of time, and in that window, the nimble, unbiased, fundamental stock picker can take advantage of overreactions and underreactions. If they don't, then the M&M propositions truly hold, and I don’t have a meaningful job. However, if this paper is right, and it is only flows that matter, then while the M&M theorems are overturned, I don't have a meaningful job either. If it is all about flows, then I shouldn't play the game.

Read More

Just How Cheap is Europe vs. the US, and Should it Be?

As it turns out, it isn’t that the people are paying a bigger growth premium for US Growth over European Growth; but instead it is that people are paying a (much) bigger multiple for US Value than for European Value.

Read More

Are American Companies Better than European Ones?

If we again go back and start the clock on January 1, 1980, and stop it thirty years later on December 31, 2009, we see that the S&P 500 generated annual total returns (with dividends) of 11.5%. During that exact same period, guess what the annual returns of the MSCI Europe were? Also 11.5%. This last decade, however, things have gotten out of whack.

Read More

Rumpelstiltskin and Meme Stock Investing

“What sort of sorcery is this?” Is this financial alchemy powering a perpetual motion engine that will result in higher and higher share prices?

Read More

Archegos, Disclosure, and Price Discovery

This had a lot to do with bad banking, but most to do with an overzealous client. Meanwhile, it had very little to do with holdings disclosure. Sure, our kneejerk reaction is (always) for more regulation, because we want to believe that some regulatory response will immediately solve all our future problems. But we should question this intuition.

Read More

It's All About the Fundies

It wasn’t passive flows that mattered. It wasn’t interest rates that mattered. It wasn’t the multiple that mattered. It wasn’t an ever-expanding infectious narrative that mattered. No analyst on the buy or sell side came remotely close to understand the market opportunity, the share, the profitability. It was about better vision, modelling. and analysis. It was all about the fundies.

Read More

On Unlimited Upside

He implies that a biased sample of self-selected winners suggest that it is a mistake to ever sell any shares in any companies that you think are “winners” either historically or prospectively. That sure would be nice, wouldn't it?

Read More

A Memo to Investors

I know, these are weird and trying times. It all makes you wonder what the point of stock-picking is. What is the purpose of kicking the tires, looking under the hood, and doing our jobs?

Read More

Investors? Possibly you!

FATMAN-G. No, that isn’t my rap name, although vaguely appropriate (I mean, the G part of course). That’s our new moniker for the Avengers[1] of the equity capital markets, to which we have now added Tesla. FATMAN-G is Facebook, Amazon, Tesla, Microsoft, Apple, Netflix, and Google.

Read More

Avengers Assemble!

Amazon is, very simply, a tremendous company. Google is also a tremendous company. The same goes for Microsoft, Apple, Netflix, and Facebook. These are the superheroes of capital markets. In these FAMANG stocks, the Avengers have assembled.

Read More

How Did This Even Happen?

No, I’m not talking about the winner of the Presidential election or COVID-19 or 2020. I’m talking about something I saw Rex Chapman tweet out over the weekend.

Read More

Was “Value” Just a Hot Hand Thing?

In 1861, at the outset of the Civil War in the United States, Union Pacific issued 20 shares in its IPO.

Read More

The Hot-Hand Fallacy Fallacy Fallacy?

Many of you will be familiar with the so-called “hot-hand” fallacy, or (perhaps) the lack thereof.

Read More

Cue the Camouflage

The S&P 500 is up 6.5% this year. That’s a total return number, and given what is going on out there, it’s pretty impressive.

Read More

The Times that Try Stock-Pickers’ Souls

On first principles, there is one way to generate excess stock market returns over the long term, and it isn’t to “own winners at any price.”

Read More

A Different Game?

I was out shooting baskets this weekend, thinking about the concept of inversion.

Read More

Heads I Win

A few months back I had a big battle with one of my oldest, most intelligent friends.

Read More

A New Ice Age?

I’ll spend $3 at the 7-11 for a bag of ice, and drop it in a cooler. I really like ice.

Read More

Grandpa Stocks

There are young companies out there that are exciting, growing quickly, and very clearly have the world in front of them.

Read More

Bubblicious?

COVID-19 and related counteractive policies have had an extremely negative impact on domestic and global economies. Whether or not you believe that the policies weren’t strong enough, or if they were overzealous, we are where we are.

Read More

On Negative Oil and Futures Prices

A quick and basic primer on spot oil prices and oil futures, and the difference between the two.

Read More

In Flew Enza

World War I began in 1914, and the US declared they would join the fight in April of 1917.

Read More

COVID-19 and Equity Markets

My wife’s family is from Tuscany, and Italian is her first language. Four years ago, she wanted to get out of London for the summer, and headed over to Italy with the kids. But instead of visiting her cousins, aunts, and uncles in Florence, she chose instead to spend 40 days in Venice.

Read More

Regulators to the Rescue?

Market authorities across many European countries have announced plans to prohibit short-selling (to varying degrees) for the foreseeable future.

Read More

Perspective

I started an investment club in college with $100. I had seven buddies that also saved $100, so we had $800 all-in.

Read More

We Don’t Make Pizzas

Here at the Albert Bridge Restaurant, the investment team has the chefs, the IR team has the waiters, and the operations team ensures that the shop runs smoothly so that we can keep on serving up alpha (hopefully) to you, our customers.

Read More

Ben Graham the Growth Investor?

We’re all for debunking myths, and given the performance of growth stocks recently, we’re making a pre-emptive strike in defense of the father of value investing.

Read More

On the Impact of the FAMANGs

Market headlines, globally, have been dominated by the storied performance of a select few transformational, winner-take-all business models.

Read More

Europe vs the US: Is it all about sector exposures?

In America’s Decade, we highlighted the very similar returns provided by the MSCI Europe and S&P 500 from 1980 through 2009, and the very different returns since.

Read More

Behavioural Finance is Finance

Last week, Barry Ritholtz had a fun interview with Eugene Fama.

Read More

America’s Decade

When it comes to predicting the economy, we believe that speculating when things will turn is an exercise in futility and a horrible waste of time; one which meanwhile distracts us all from the task at hand.

Read More

Known Unknowns and Share Prices

In February of 2002, Donald Rumsfeld famously introduced known knowns, known unknowns, and unknown unknowns into the lexicon.

Read More

Prediction, Publicity, and Paul the Octopus

Unlike many other market observers, we just don’t see the point in discussing or debating the macroeconomics driving overall markets, volatility, or sentiment.

Read More

Are Company Visits Good or Bad?

Our most profitable investment, ever, was probably the combined result of a lotta luck, some skill, and hard work.

Read More

Everybody Was Kung Fu Fighting?

Last week, Finance Twitter erupted over a Bloomberg article about Michael Burry [i] and how he likened passive investment in equity markets to the bubble in the synthetic CDO market back in 2007, which he famously – thanks to Michael Lewis and Christian Bale – identified.

Read More

Voting Machines and Weighing Machines

Ben Graham is famously attributed for stating that the market was a voting machine in the short term, but a weighing machine in the long term.

Read More

The DCF is the Randy Watson of Valuation

I’m not very well-rounded. I studied finance in college, and finance in business school.

Read More

The Sacrilegious Diaries: Measuring the Impact of Portfolio Turnover

A few weeks ago, we discussed the potential benefits of portfolio and name turnover.

Read More

Imagine No Inflation

Many folks have now listened to this fascinating interview of the pseudonymous Jesse Livermore by Patrick O’Shaughnessy.

Read More

The Sacrilegious Diaries: The Benefits of Turnover

For a fundamental, value-oriented investor, we are reasonably active in the management of our portfolio names.

Read More

Stay in the Game

This is going to be an uncharacteristic departure for me. This story is deeply personal, for our family, and for our oldest son in particular.

Read More

I’m Volatility?

Is risk “volatility vs. a benchmark” or is risk “the potential permanent loss of capital”?

Read More

Woody was Right

If you are managing a portfolio of equity investments, whether personally or institutionally, there are many factors that (should) go into its construction.

Read More

When You Can’t Wait For Tomorrow

We’re mulling this morning over what it is that makes stock prices, and stock-picking, work.

Read More

James Harden and Alpha

I played high school basketball in Indiana. I won a few honors, but was broadly mediocre, and certainly not NCAA D1 material.

Read More

Groundhog Day and Overnight Returns

Over the past few years, some of the finance literature has started addressing the phenomenon, if not the apparent puzzle, of overnight returns (close-to-open) vs. intraday returns (open-to-close).

Read More

The Right Way

We wanted to quickly highlight that the difference between the fee structure of a large, diversified, purportedly active fund and a smaller, concentrated, active fund.

Read More

The First Step to Regaining Credibility

As equity indices romped higher throughout most of the last ten years, the long-short hedge fund industry increasingly came under attack.

Read More

The Futility of Market Timing

We are not big fans of market timing. Those that profess to have such a skill before the fact often always turn out not to have had much skill in hindsight.

Read More

Visualizing the Arithmetic of Active Management

It’s been said that a picture can be worth a thousand words.

Read More

Sweet Emotion?

No matter what we pretend to ourselves, even for those of us with more than ten years of investing experience, this move is painful.

Read More

Share Buybacks, Bad Companies, and Bear Markets

The star has fallen for a few companies out there, and for those that had previous share buyback programs, there have been some of the predictable “see I told you so” articles written about them.

Read More

Risk and Portfolio Theory

As we’ve discussed, efficient market academia suggests that Mr. Market actually only cares about systematic risk.

Read More

Reminiscences of a Stock Operator: The Volkswagen Chronicles, Ten Years Later

In the spring of 2008, things were already wacky at Volkswagen.

Read More

We’d Rather Not Sleep

There is a tilt in our portfolio toward value stories where we think the consensus investor is biased against processing improving fundamentals.

Read More

Factor Timing, Should You Try?

These are our two cents on whether you, or we, or anyone else can pick the perfect time.

Read More

The Mathematics of Maintaining Bet Size

We aren’t big fans of dipping our toes in the water when entering a position, nor of timidly reducing when exiting.

Read More

The Grandfather of Behavioural Investing

Benjamin Graham is considered by many as a founding father of value investing.

Read More

On Sexual Chocolate and Semi-Annual Reporting

The presupposition that quarterly earnings and guidance somehow breeds short-termism and suboptimal business strategy,

Read More

Island Economies and Risk

In this economy there are two companies, a resort hotel, and an umbrella manufacturer.

Read More

Build a Bear?

Imagine every adult has 10% of their savings invested in “the global stock market”,

Read More

Data Science and Alpha

As the investment community embraces data science, we should not be blind to the reality that many of our active-management peers are

Read More

Hunting for Alpha

But Can a Stock-Picker Really Generate Alpha, and is it Luck or Skill When it Happens?

Read More

Career Risk, Alpha, and Contrarian Investing

At our firm, one of our main goals is, very simply, to generate excess returns from equity investing without taking commensurate risks.

Read More

Passive Flows and Wheelbarrows

A nightly sort of the most active US names is usually dominated by ETFs. Earlier this month, we took a peek at the most heavily traded names on one particular day.

Read More

God Bless the Shorts

Elon Musk made a lot of news last week, refusing to answer “boneheaded” questions from “boring” sell-side analysts.

Read More

Equilibrium Happens

There is a great deal of discussion these days regarding the impact of passive investing

Read More

Peak Quality?

Mr. Market has been increasingly attracted to and enamoured by the concept of “quality” investing. So, let’s explore it.

Read More

Bill Sharpe and Hank Aaron

We basically need to hold something different (either securities or bet sizes) than the “market”.

Read More

Unwarrented

Evidently, the closest thing we in financial markets have to Albert Einstein or Winston Churchill, is Warren Buffett.

Read More

The Search for Excellence and the Loser’s Game

We’re on a continual search for the very best ideas for our concentrated portfolio.

Read More

Fooled by Non-Randomness

Students of decision-making and bias will all have seen the work by Cornell psychologist Tom Gilovich,

Read More

Half Hearted Is Half Minded

After discovering the next great investment idea, why is it so easy to start with a half-sized position, watch it a bit, and then go full-sized later?

Read More

122 year Dow Jones Histogram: Putting 2017 into context

2017 was a pretty good year for the stock market. The 19th best since the Dow Jones Average was introduced in 1896.

Read More

Pegs, P/E'S and the Value Premium

The notion that the PEG is a linear tool for valuation is a myth, and a deeper analysis of its function reveals that the difference in outperformance of growth stocks over value stocks accelerates as interest rates drop toward zero.

Read More

Rick Barry and Lewis Carroll

The goal of our business, very simply, is to generate excess returns for our investors without taking commensurate risks.

Read More

Secular Winners and Value Investing

There are very few growth investors that stayed in business long enough to become a household name in the investment community, and even less of them that ended up writing books about their lifetime experiences.

Read More

On Passive Flows, Smart Money, and Alpha

The trend from active to passive (or systematic) investing is now well-entrenched.

Read More